Dell Technologies Q1 FY2027 Earnings Preview: AI Server Growth Meets the Margin Test

Dell enters its May 28, 2026 earnings release with unusually high expectations: roughly $35 billion-plus in quarterly revenue, nearly doubled adjusted EPS from a year ago, and investors focused less on “can AI servers grow?” than on “can AI servers grow profitably?”

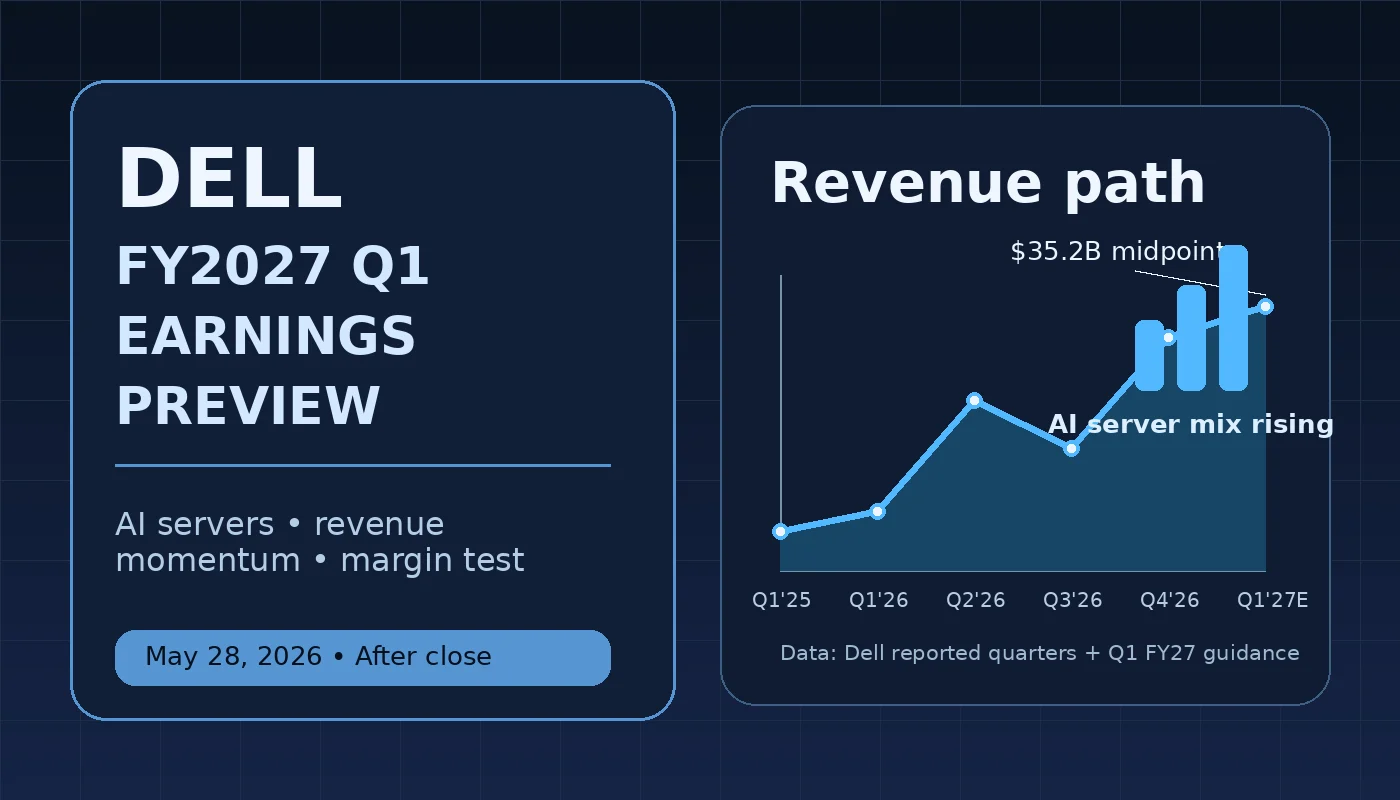

Dell Technologies is scheduled to report fiscal 2027 first-quarter results on Thursday, May 28, 2026 after the U.S. market close, with the company’s investor event listed for 3:30 p.m. CDT. The setup is not subtle. Dell’s own guidance implies a step-change quarter, while third-party consensus sits near the high end of management’s range.

This is a general market analysis based on public information available before the release. It is not investment advice.

The number to beat

Dell’s official Q1 FY2027 guidance is the cleanest starting point. In its fiscal 2026 fourth-quarter release, the company guided for Q1 FY2027 revenue of $34.7 billion to $35.7 billion, with a midpoint of $35.2 billion, up about 51% year over year. Dell also guided for GAAP diluted EPS of $2.55 at the midpoint and non-GAAP diluted EPS of $2.90 at the midpoint, up about 87% year over year.

Third-party expectations are a little higher. MarketBeat listed consensus EPS of $2.96 and expected revenue of $35.74 billion for Q1 FY2027. Tastylive, citing TradingView, showed the same broad setup: $2.96 EPS on $35.74 billion revenue, compared with $1.55 EPS on $23.38 billion revenue a year ago.

| Metric | Dell official Q1 FY2027 guidance | Current consensus snapshot | Year-ago Q1 FY2026 actual | What it means |

|---|---|---|---|---|

| Revenue | $34.7B–$35.7B; midpoint $35.2B | ~$35.74B | $23.38B | Revenue is expected to rise about 51%–53% year over year. |

| Non-GAAP diluted EPS | $2.90 midpoint, plus/minus $0.10 | ~$2.96 | $1.55 | Adjusted EPS is expected to nearly double from last year. |

| GAAP diluted EPS | $2.55 midpoint | Not the main Street focus | $1.37 | GAAP profit growth should still be very strong. |

| FY2027 revenue guide | $138B–$142B | Investors will watch for any raise | FY2026 actual: $113.5B | The full-year guide is the bigger stock-moving variable. |

| FY2027 AI-optimized server revenue guide | Roughly $50B | No single consensus benchmark | FY2026 AI-optimized server revenue: $24.7B | The AI server business is now large enough to define the whole Dell story. |

Sources: Dell Q4 FY2026 and FY2027 guidance release, MarketBeat Q1 FY2027 earnings page, tastylive earnings preview.

The prior-results comparison: Dell’s business has changed shape

The most important comparison is not only Q1 FY2027 versus Q1 FY2026. It is Q1 FY2027 versus the Dell of two years ago.

In Q1 FY2025, Dell reported $22.24 billion of revenue. ISG, the infrastructure segment that includes servers, storage, and networking, contributed $9.23 billion. By Q4 FY2026, total revenue had reached $33.38 billion, and ISG alone produced $19.60 billion. In plain English: Dell’s infrastructure business has moved from being an important segment to being the center of the equity story.

| Quarter | Revenue | YoY revenue growth | Non-GAAP EPS | ISG revenue | CSG revenue | Read-through |

|---|---|---|---|---|---|---|

| Q1 FY2025 | $22.24B | 6% | $1.27 | $9.23B | $11.97B | AI was visible, but Dell was still much more balanced between PCs and infrastructure. |

| Q1 FY2026 | $23.38B | 5% | $1.55 | $10.32B | $12.51B | Revenue growth was modest, but AI server demand was already reshaping expectations. |

| Q2 FY2026 | $29.78B | 19% | $2.32 | $16.80B | $12.50B | AI shipments drove a major ISG acceleration. |

| Q3 FY2026 | $27.01B | 11% | $2.59 | $14.11B | $12.48B | Revenue dipped sequentially, but profitability kept improving. |

| Q4 FY2026 | $33.38B | 39% | $3.89 | $19.60B | $13.49B | AI-optimized servers became a quarter-defining business line. |

| Q1 FY2027 guide midpoint | $35.20B | ~51% | $2.90 | Not separately guided in release | Not separately guided in release | The quarter is expected to exceed Q4 revenue, though EPS is guided below Q4’s seasonally strong level. |

Sources: Dell Q1 FY2025 release, Dell Q1 FY2026 release, Dell Q2 FY2026 release, Dell Q3 FY2026 release, Dell Q4 FY2026 release.

Two details stand out.

First, Dell’s Q1 FY2027 revenue guide implies about 5.5% sequential growth from Q4 FY2026, even though Q4 is usually a strong quarter. That is not normal seasonal drift. It reflects a backlog and shipment cycle tied to AI infrastructure.

Second, the non-GAAP EPS guide of $2.90 is about 25% below Q4 FY2026’s $3.89, even though revenue is guided higher. That gap is the margin story. Dell can grow revenue very quickly with AI servers, but the market wants proof that AI revenue can produce durable operating profit, not only impressive top-line volume.

Why AI servers are the center of the print

Dell closed fiscal 2026 with record full-year revenue of $113.5 billion, up 19%, and said it had closed more than $64 billion in AI-optimized server orders, shipped more than $25 billion, and entered fiscal 2027 with $43 billion of AI backlog.

The Q4 segment data shows how fast the mix changed. In Q4 FY2026, Dell reported:

- AI-optimized server revenue: $8.95 billion, up 342% year over year.

- Traditional servers and networking revenue: $5.85 billion, up 27%.

- Storage revenue: $4.80 billion, up 2%.

- Total ISG revenue: $19.60 billion, up 73%.

That means AI-optimized servers were roughly 27% of total company revenue and about 46% of ISG revenue in Q4 FY2026. For Q1 FY2027, management’s earnings-call commentary pointed to about $13 billion of AI server revenue supporting ISG growth of more than 100%. If Dell lands near that figure, AI servers would represent roughly 37% of total company revenue at the official Q1 revenue midpoint.

That is why the print will not be judged like a normal PC-and-server quarter. Dell is being tested as an AI infrastructure supplier.

Sources: Dell Q4 FY2026 release, Alpha Spread transcript of Dell Q4 FY2026 earnings call.

The margin test is the real earnings story

The bullish case is easy to understand: Dell has an enormous AI backlog, deep enterprise relationships, supply-chain scale, and a broad portfolio around servers, storage, networking, services, and workstations.

The harder question is quality of growth.

AI server revenue can be lower-margin than traditional enterprise infrastructure because large accelerator-heavy deals carry expensive components, fast-changing configurations, and customer concentration risk. Dell management has repeatedly pointed to mid-single-digit operating margins in the AI server business and has said pricing actions are being used to offset rising input costs, especially memory.

That makes four items especially important in the Q1 FY2027 report:

- AI server revenue and backlog. A revenue beat matters more if backlog and pipeline remain strong after shipments.

- ISG operating margin. Investors will watch whether the Q4 margin rebound was sustainable as AI mix rises.

- CSG margin recovery. Dell’s PC/client business grew in Q4, but management also acknowledged aggressive share capture and margin pressure.

- Q2 and full-year guidance. With the stock already pricing in a major AI infrastructure cycle, a merely “good” Q1 may not be enough without stronger forward guidance.

CSG still matters, but it is no longer the headline

Client Solutions Group (CSG), Dell’s PC, workstation, and client-device business, is not irrelevant. In fact, it still generated $13.49 billion of revenue in Q4 FY2026. Commercial client revenue rose 16% year over year, while consumer revenue was roughly flat.

But CSG is no longer the main growth engine. In Q1 FY2025, CSG revenue of about $12.0 billion was larger than ISG revenue of $9.2 billion. By Q4 FY2026, ISG revenue was about 45% larger than CSG revenue.

For Q1 FY2027, the investor question is not whether PCs return to hypergrowth. It is whether CSG can hold or improve profitability while Dell allocates investor attention, supply-chain resources, and capital-market credibility toward AI infrastructure.

What would count as a strong report?

A clean beat would probably need more than revenue above $35.7 billion. The stronger version of the report would include:

- Revenue above the high end of Dell’s guidance range.

- Non-GAAP EPS above the $2.90–$3.00 zone.

- AI server revenue at or above the roughly $13 billion expectation.

- Stable or improving ISG operating margin despite AI mix.

- Backlog that remains healthy after heavy shipments.

- Q2 guidance that shows the AI ramp is continuing, not simply pulling demand forward.

- Any upward revision to the FY2027 revenue or AI server revenue outlook.

A weaker report could still show huge year-over-year growth. That is the strange part. If the stock has already moved on AI optimism, the market may punish a result that is fundamentally strong but strategically less exciting: a modest beat, lower margin quality, backlog drawdown, or conservative forward commentary.

Bottom line

Dell’s Q1 FY2027 earnings report is a growth test, but even more, it is a credibility test for the AI infrastructure cycle.

The company has already shown that AI servers can transform revenue. The next question is whether Dell can turn that demand into durable profit, cash flow, and guidance momentum. Compared with the last several quarters, the bar is much higher now: Q1 FY2026 was about proving AI demand existed; Q1 FY2027 is about proving AI scale works.

FAQ

When will Dell report Q1 FY2027 earnings?

Dell Technologies is scheduled to discuss fiscal 2027 first-quarter results on May 28, 2026, with its investor event listed for 3:30 p.m. CDT. Market earnings calendars classify the report as after the U.S. market close.

What are analysts expecting from Dell’s Q1 FY2027 earnings?

Current third-party consensus snapshots cluster around $35.7 billion of revenue and $2.96 adjusted EPS, while Dell’s own guidance midpoint is $35.2 billion of revenue and $2.90 non-GAAP EPS.

How does Q1 FY2027 compare with Q1 FY2026?

Dell’s Q1 FY2026 revenue was $23.38 billion, with $1.55 non-GAAP EPS. The Q1 FY2027 guidance midpoint implies roughly 51% revenue growth and about 87% non-GAAP EPS growth year over year.

What is the most important segment to watch?

Infrastructure Solutions Group (ISG) is the key segment because it contains Dell’s AI-optimized server business. In Q4 FY2026, ISG revenue rose 73% year over year to $19.6 billion, driven by AI-optimized servers.

Why could the stock fall even if Dell beats expectations?

The stock has rallied sharply into the print, so investors may demand more than a headline beat. Margin quality, backlog durability, AI server profitability, and forward guidance could matter more than Q1 revenue alone.

Sources

- Dell Technologies Fiscal Year 2027 First Quarter Results event page — Dell Technologies Investor Relations, May 28, 2026. Used for: event timing.

- Dell Technologies Delivers Fourth Quarter and Full-Year Fiscal 2026 Results — Dell Technologies Investor Relations, February 26, 2026. Used for: Q4 FY2026 actuals, FY2027 guidance, AI server metrics.

- Dell Technologies Delivers Third Quarter Fiscal 2026 Financial Results — Dell Technologies Investor Relations, November 25, 2025. Used for: Q3 FY2026 comparison.

- Dell Technologies Delivers Second Quarter Fiscal 2026 Financial Results — Dell Technologies Investor Relations, August 28, 2025. Used for: Q2 FY2026 comparison.

- Dell Technologies Delivers First Quarter Fiscal 2026 Financial Results — Dell Technologies Investor Relations, May 29, 2025. Used for: Q1 FY2026 comparison.

- Dell Technologies Delivers First Quarter Fiscal 2025 Financial Results — Dell Technologies Investor Relations, May 30, 2024. Used for: Q1 FY2025 comparison.

- Dell Technologies Q1 2027 Earnings Report — MarketBeat, May 28, 2026. Used for: consensus EPS/revenue and after-close classification.

- Dell Earnings Preview: Can Dell Climb Higher on AI Strength? — tastylive, May 27, 2026. Used for: TradingView consensus snapshot, market setup, options-implied move.

- DELL Q4-2026 Earnings Call — Alpha Spread transcript, February 26, 2026. Used for: Q1 FY2027 segment-level commentary and margin discussion.