Oracle’s AI Repricing: Why the Stock Fell, Why It Rebounded, and What Stargate Means for Debt Risk

Oracle did not fall because investors suddenly stopped believing in AI. It fell because Oracle’s AI story started to look like a leveraged infrastructure buildout. The rebound came when the company showed that AI demand was converting into real cloud revenue faster than skeptics feared.

This article is general financial analysis based on public information available as of May 29, 2026. It is not investment advice.

The simplest read

Oracle became one of the market’s most dramatic AI infrastructure stories in 2025 and 2026. Investors first rewarded the company for landing huge AI cloud commitments. Then they punished it for the cost of delivering those commitments.

That tension is the whole story.

Oracle’s cloud backlog, measured by remaining performance obligations, exploded from a level typical of a mature enterprise software company into something closer to a hyperscale infrastructure pipeline. In September 2025, Oracle said Q1 fiscal 2026 remaining performance obligations rose 359% year over year to $455 billion, helped by four multi-billion-dollar contracts with three customers. Management also previewed a sharply higher Oracle Cloud Infrastructure revenue roadmap, including expected OCI revenue of $18 billion in fiscal 2026 and much higher figures in later years. Oracle Q1 FY2026 results

But backlog is not cash in the bank. To turn AI contracts into revenue, Oracle has to build or lease data centers, secure power, install chips, finance construction, and deliver capacity on time. That is why the same AI demand that made the stock exciting also made investors nervous.

What happened to Oracle’s stock?

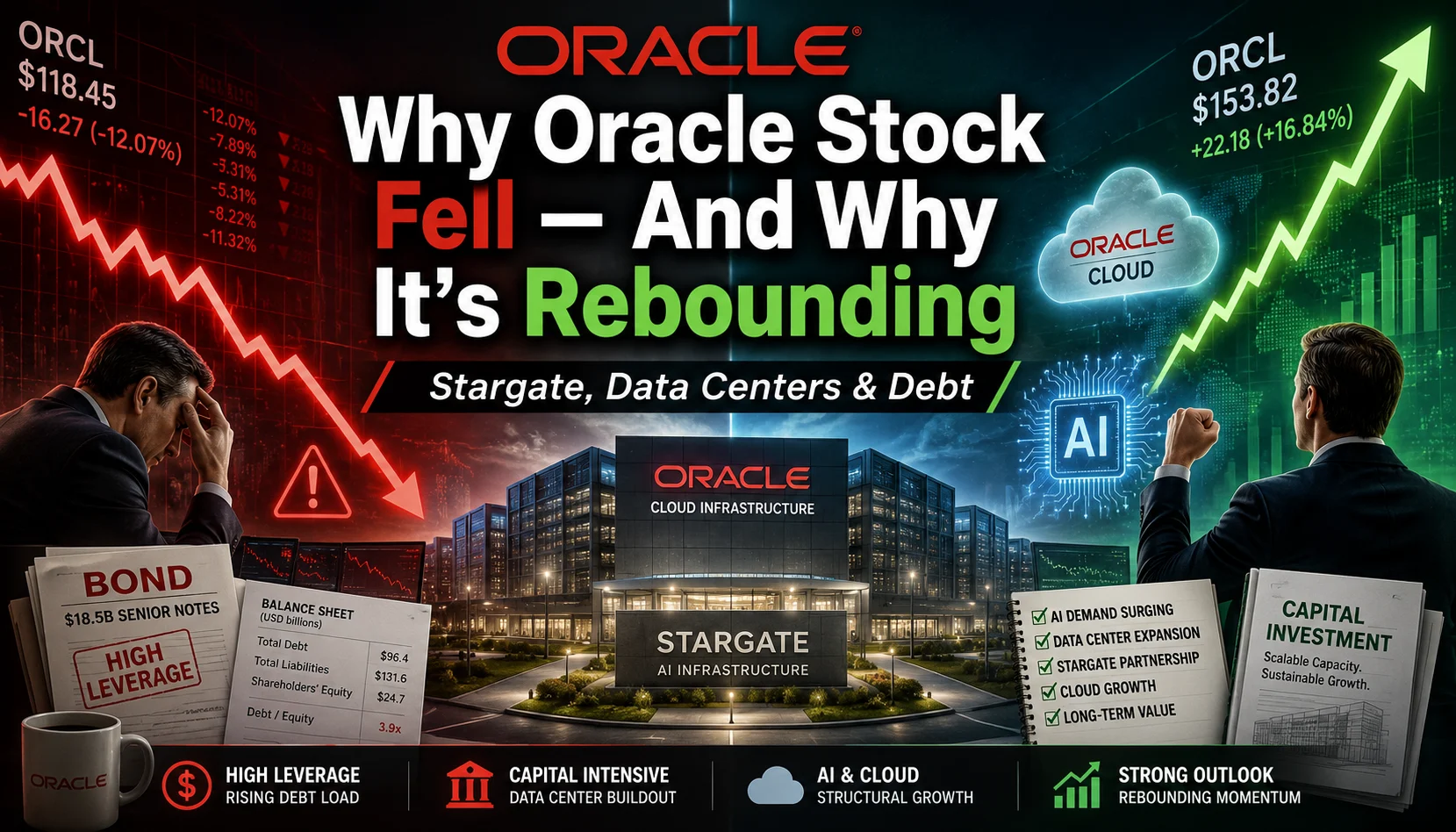

Oracle’s stock surged after the September 2025 backlog announcement. Reuters later described that move as a “stunning 36% jump” after Oracle announced its massive booked cloud orders. By December, that enthusiasm had faded as investors focused on OpenAI exposure, debt, and the financial implications of the data-center buildout. Reuters, Dec. 9, 2025

The clearest shock came after Q2 fiscal 2026. Oracle reported strong headline numbers, including $16.1 billion in quarterly revenue and $523 billion in remaining performance obligations, but investors focused on weaker-than-hoped forecasts and a much larger capital spending burden. Reuters reported that Oracle shares sank 13% on December 11, 2025, as higher spending and gloomy forecasts raised doubts over how quickly AI investments would pay off. Oracle Q2 FY2026 results, Reuters, Dec. 11, 2025

The recent rebound has not erased all concerns, but it changed the tone. In March 2026, Oracle’s Q3 results showed faster revenue growth, a larger backlog, and management reassurance on funding. Reuters reported that Oracle shares rose 8.3% in extended trading after the company predicted AI data-center demand would lift revenue above Wall Street expectations into fiscal 2027. Reuters, Mar. 10, 2026

Why Oracle stock fell so much

1. The market started treating Oracle like an infrastructure borrower, not just a software company

Oracle’s old identity was simple: enterprise database, applications, support revenue, and durable cash generation. The new AI story is different. It requires enormous upfront investment before the revenue arrives.

In its Q3 fiscal 2026 filing, Oracle said cash used for capital expenditures rose to $39.2 billion in the first nine months of fiscal 2026, up from $12.1 billion in the same period of fiscal 2025, primarily because of data-center expansion. Oracle also said it expected the upward capex trend to continue as it expands existing data centers and establishes new sites. Oracle FY2026 Q3 Form 10-Q

That is a major change in the cash-flow profile. It makes Oracle more sensitive to construction delays, power availability, chip supply, interest rates, and customer payment timing.

2. The backlog was huge, but investors questioned its quality and timing

Remaining performance obligations, or RPO, represent contracted revenue that has not yet been recognized. Oracle’s RPO reached $523 billion in Q2 and $552.6 billion by the end of Q3 fiscal 2026. The Q3 filing said Oracle expected to recognize about 12% of that RPO as revenue over the next twelve months, 31% over months 13 to 36, 35% over months 37 to 60, and the remainder later. Oracle FY2026 Q3 Form 10-Q

That schedule matters. A giant backlog can support a bullish long-term story, but it does not automatically solve short-term funding pressure. Oracle may have to spend heavily today while recognizing much of the revenue over several years.

3. OpenAI concentration made the story feel fragile

The OpenAI relationship is central to Oracle’s AI narrative. Reuters reported in December 2025 that Oracle had vaulted into the AI infrastructure race thanks to a roughly $300 billion OpenAI deal, but that the pact also tethered Oracle’s fortunes to the ChatGPT maker. Investors worried because OpenAI, while strategically important, was still unprofitable and had not fully detailed how it would finance its enormous infrastructure plans. Reuters, Dec. 11, 2025, Reuters, Dec. 9, 2025

This does not mean the OpenAI contract is bad. It means the market assigned a higher risk premium to Oracle because one customer ecosystem became so important to the growth story.

4. Debt, leases, and power commitments became the center of the debate

Oracle’s Q3 fiscal 2026 10-Q shows why credit investors became alert. As of February 28, 2026, Oracle had $130.9 billion of senior notes and other long-term borrowings outstanding. During the first nine months of fiscal 2026, it issued $43.0 billion of senior notes. It also disclosed $261 billion of additional lease commitments, substantially all related to data-center arrangements, generally expected to begin between Q4 fiscal 2026 and fiscal 2028 for terms of fifteen to nineteen years. Separately, Oracle reported $11 billion of unconditional purchase and other obligations, primarily related to data-center power arrangements. Oracle FY2026 Q3 Form 10-Q

The important nuance: lease commitments are not exactly the same as funded debt today. But economically, they are still long-duration obligations that can create fixed-cost pressure if demand ramps slower than expected.

5. Data-center execution risk became visible

AI data centers are not software downloads. They need land, power, cooling, permitting, chips, construction labor, grid interconnection, financing, and operating expertise.

In December 2025, Reuters reported that Oracle denied a Bloomberg report that some OpenAI-related data centers had been delayed to 2028 because of labor and material shortages. Oracle said there were no delays to sites required to meet contractual commitments and that milestones remained on track. The market reaction still mattered: Oracle shares fell after the report before paring some losses. Reuters, Dec. 12, 2025

A few days later, Reuters reported that Oracle said talks for a Michigan data-center equity deal remained on schedule after a report of stalled negotiations knocked the stock down 5%. The project was described as a more than 1-gigawatt Stargate-related site in Saline Township, Michigan. Reuters, Dec. 17, 2025

These reports show the market’s sensitivity. Even when Oracle pushes back, investors now treat every data-center headline as a potential signal about funding, timing, and margins.

Why Oracle stock rebounded

1. Q3 showed that AI demand was converting into revenue

The rebound began because Q3 fiscal 2026 looked meaningfully better than the fear case. Oracle reported total revenue of $17.2 billion, up 22% year over year. Cloud revenue rose 44% to $8.9 billion, and Oracle Cloud Infrastructure revenue rose 84% to $4.9 billion. Remaining performance obligations reached $553 billion, up 325% year over year. Oracle Q3 FY2026 results

That is the single most important reason for the rebound. The market needed evidence that Oracle’s AI contracts were not just press-release backlog. Q3 showed accelerating OCI revenue.

2. Management gave a clearer funding message

Oracle said in Q3 that most of the quarter’s RPO increase related to large-scale AI contracts where it did not expect to raise incremental funds because much of the needed equipment was either funded upfront through customer prepayments or purchased and supplied by the customer. Oracle also said it had raised $30 billion within days through investment-grade bonds and mandatory convertible preferred stock after announcing plans to raise up to $50 billion in debt and equity financing. Oracle Q3 FY2026 results

Reuters separately reported that Oracle expected to raise $45 billion to $50 billion in 2026 to build additional cloud infrastructure capacity, using a mix of debt and equity. About half was expected through equity-linked and common-equity instruments, including mandatory convertible preferred securities and an at-the-market equity program of up to $20 billion, with the other half through senior unsecured bonds. Reuters, Feb. 1, 2026

That did not eliminate dilution or leverage risk. It did reduce the fear of a near-term funding scramble.

3. Fiscal 2027 guidance gave bulls a new anchor

Oracle maintained fiscal 2026 revenue guidance of $67 billion and capex guidance of $50 billion, while raising fiscal 2027 revenue guidance to $90 billion. Reuters reported that the fiscal 2027 forecast was above the $86.6 billion estimate compiled by LSEG. Oracle Q3 FY2026 results, Reuters, Mar. 10, 2026

The market does not need every risk to disappear for a stock to rebound. It only needs the base case to look less broken than the bear case. Q3 did that.

4. Broader AI sentiment improved

Oracle also benefited from a stronger AI tape. By late May 2026, Reuters reported that the S&P 500 and Nasdaq hit record closing highs as AI-fueled optimism offset other concerns, with semiconductor stocks leading gains. Oracle is not a semiconductor stock, but its AI infrastructure story sits in the same market narrative. Reuters, May 26, 2026

When investors become more willing to pay for AI infrastructure growth, Oracle’s backlog becomes an asset again rather than only a liability.

Stargate: opportunity and risk in the same package

The Stargate Project is the centerpiece of Oracle’s new AI identity. OpenAI announced the project on January 21, 2025, saying it intended to invest $500 billion over four years to build AI infrastructure for OpenAI in the United States, with $100 billion to be deployed immediately. Initial equity funders included SoftBank, OpenAI, Oracle, and MGX; SoftBank had financial responsibility, OpenAI had operational responsibility, and key technology partners included Arm, Microsoft, NVIDIA, Oracle, and OpenAI. OpenAI, Jan. 21, 2025

In September 2025, OpenAI, Oracle, and SoftBank announced five new U.S. AI data-center sites. OpenAI said the new sites, plus the flagship Abilene, Texas site and ongoing CoreWeave projects, brought Stargate to nearly 7 gigawatts of planned capacity and more than $400 billion of investment over the next three years. OpenAI also said its July agreement with Oracle to develop up to 4.5 gigawatts of additional Stargate capacity represented a partnership exceeding $300 billion over five years. OpenAI, Sept. 23, 2025

For Oracle, Stargate is powerful because it can turn OCI into core AI infrastructure rather than a distant third or fourth cloud option. But it is risky because the investment cycle is brutally front-loaded. Oracle has to commit capital, leases, and power before all revenue is recognized.

There is also a distinction investors should keep clear: “Stargate” is not one single clean line item. It includes a high-profile strategic initiative, bilateral Oracle-OpenAI capacity agreements, site-level financing, leasing structures, data-center developers, power arrangements, and chip procurement. A delay or change at one site does not automatically kill the entire project, but it can change the timing and economics.

That nuance appeared in March 2026. Reuters reported that Bloomberg said Oracle and OpenAI had abandoned plans to expand a flagship AI data center in Texas after negotiations over financing and OpenAI’s changing needs. But Reuters also cited a source saying the capacity would be fulfilled at another campus, that two of eight Abilene buildings were already up and running, and that the Oracle-OpenAI plan to develop another 4.5 gigawatts of capacity remained on track. Reuters, Mar. 6, 2026

The takeaway: Stargate is real enough to move Oracle’s numbers, but messy enough to keep risk premiums elevated.

Debt issue analysis: what matters most

| Issue | Current fact | Why it matters |

|---|---|---|

| Senior notes and long-term borrowings | $130.9 billion outstanding as of February 28, 2026 | Higher leverage makes Oracle more sensitive to rates, ratings, and cash-flow timing. |

| New senior notes | $43.0 billion issued in the first nine months of fiscal 2026 | Oracle is actively using debt to fund the AI buildout. |

| Capital expenditures | $39.2 billion in the first nine months of fiscal 2026, up from $12.1 billion a year earlier | Capex is moving faster than traditional software-company cash-flow expectations. |

| Additional lease commitments | $261 billion, mostly data-center related, not yet reflected on the balance sheet | Future fixed obligations can pressure free cash flow if demand or margins disappoint. |

| Power and other obligations | $11 billion, primarily data-center power arrangements | AI capacity is constrained by electricity, not only chips. |

| Funding plan | Up to $50 billion in debt and equity financing; $5 billion mandatory convertible preferred stock issued; up to $20 billion ATM equity program authorized but not used as of February 28, 2026 | Funding visibility improved, but dilution and leverage remain part of the story. |

| RPO | $552.6 billion as of February 28, 2026 | A large backlog supports the bull case, but revenue recognition stretches across years. |

Source: Oracle FY2026 Q3 Form 10-Q

The debt question is not simply “Can Oracle pay its debt?” Oracle remains a large, profitable company with deep enterprise relationships. The sharper question is whether the incremental AI infrastructure business earns attractive returns after interest expense, data-center leases, power, depreciation, chip costs, customer concentration, and execution delays.

If the answer is yes, Oracle’s current investment cycle could look like a bold but rational land grab. If the answer is no, the same commitments could become a long-duration drag on free cash flow.

What investors should watch next

The cleanest way to track Oracle is not to argue about AI hype in the abstract. Watch the conversion mechanics.

First, watch OCI revenue growth relative to capex. If OCI keeps accelerating while capex stabilizes, the bull case improves. If capex keeps rising faster than revenue, the market will question returns.

Second, watch RPO quality. The headline number matters less than the mix of customers, prepayments, cancellation terms, recognition timing, and margin profile.

Third, watch free cash flow. Operating cash flow can look strong while free cash flow suffers because data-center capex is enormous. Oracle’s Q3 filing showed $17.4 billion of cash inflows from operations in the first nine months of fiscal 2026, but $39.2 billion of cash used for capital expenditures in the same period. Oracle FY2026 Q3 Form 10-Q

Fourth, watch lease commitments. A rising lease-commitment line can be just as important as debt issuance because future fixed obligations shape the risk profile.

Fifth, watch Stargate site milestones. The important signal is not whether every announced site proceeds exactly as first described. The signal is whether total contracted capacity comes online on time, at acceptable cost, with customers paying as expected.

Bottom line

Oracle’s selloff and rebound are two sides of the same trade.

The selloff happened because investors realized Oracle’s AI growth is not a low-capex software upgrade. It is a massive infrastructure cycle tied to OpenAI, Stargate, debt markets, data-center leases, power constraints, and long construction timelines.

The rebound happened because Q3 fiscal 2026 showed that demand is not imaginary. OCI revenue accelerated, RPO hit another record, management raised fiscal 2027 revenue guidance, and Oracle offered a more credible funding path.

So the right framing is not “Oracle is an AI winner” or “Oracle is a debt bubble.” The real question is narrower and more useful: can Oracle convert its AI backlog into high-margin cloud revenue before fixed obligations and financing costs eat the upside?

That is the race Oracle is running now.

FAQ

Why did Oracle stock fall so much?

Oracle stock fell because investors became worried about the cost and timing of its AI data-center buildout. The main concerns were higher capex, rising debt, large lease commitments, OpenAI concentration, and uncertainty around when AI contracts would turn into profitable cash flow.

Why did Oracle stock rebound recently?

Oracle rebounded after Q3 fiscal 2026 results showed stronger-than-expected revenue growth, 84% year-over-year Oracle Cloud Infrastructure growth, record $553 billion RPO, and raised fiscal 2027 revenue guidance. The company also reassured investors that many new AI contracts would not require incremental funding because of customer prepayments or customer-supplied GPUs.

What is Stargate, and why does it matter for Oracle?

Stargate is a large AI infrastructure initiative involving OpenAI, SoftBank, Oracle, and MGX. It matters because it positions Oracle Cloud Infrastructure as a major supplier of compute for OpenAI and related AI workloads. It also matters because building that capacity requires huge capital, leases, power arrangements, and execution discipline.

Is Oracle’s debt problem fatal?

Not based on public information alone. Oracle is still a large, profitable company, and it has raised capital successfully. The risk is not immediate insolvency; the risk is that capex, leases, interest expense, and execution delays reduce free cash flow or dilute shareholders before the AI revenue stream fully matures.

What single metric matters most now?

OCI revenue growth relative to capex is the most practical metric. If Oracle can keep converting backlog into fast-growing cloud revenue while capex eventually moderates, the bull case strengthens. If capex and lease obligations keep rising faster than realized revenue and cash flow, the bear case returns.

Sources

- Oracle Announces Fiscal Year 2026 First Quarter Financial Results — Oracle, September 9, 2025. Used for Q1 RPO and OCI roadmap.

- Oracle Announces Fiscal Year 2026 Second Quarter Financial Results — Oracle, December 10, 2025. Used for Q2 revenue, cloud revenue, and RPO.

- Oracle Announces Fiscal Year 2026 Third Quarter Financial Results — Oracle, March 10, 2026. Used for Q3 revenue, OCI growth, RPO, guidance, and funding commentary.

- Oracle FY2026 Q3 Form 10-Q — SEC filing, filed March 2026. Used for debt, lease commitments, capex, power obligations, RPO recognition schedule, and cash-flow data.

- Announcing The Stargate Project — OpenAI, January 21, 2025. Used for Stargate structure, initial funders, and investment plan.

- OpenAI, Oracle, and SoftBank expand Stargate with five new AI data center sites — OpenAI, September 23, 2025. Used for Stargate capacity, investment scale, sites, and Oracle-OpenAI capacity agreement.

- Oracle’s OpenAI reliance faces scrutiny as debt-fueled AI buildout raises worries — Reuters, December 2025. Used for market concerns around OpenAI exposure, debt, and stock reaction.

- Oracle slumps as gloomy forecasts, soaring spending fan AI bubble worries — Reuters, December 2025. Used for the December selloff and AI-spending concerns.

- Oracle denies report on OpenAI data center delays — Reuters, December 2025. Used for data-center delay concerns and Oracle’s response.

- Oracle says Michigan data center project talks on track without Blue Owl — Reuters, December 2025. Used for Michigan project and financing concerns.

- Oracle says it plans to raise up to $50 billion in debt and equity this year — Reuters, February 2026. Used for the financing plan.

- Oracle sees AI boom through at least 2027, sending shares up 8% — Reuters, March 2026. Used for rebound, Q3 market reaction, and fiscal 2027 guidance context.

- Oracle and OpenAI drop Texas data center expansion plan, Bloomberg News reports — Reuters, March 2026. Used for Abilene expansion context and on-track 4.5GW claim.

- S&P 500, Nasdaq hit record closing highs on AI optimism — Reuters, May 2026. Used for broader AI market sentiment.